State-Dependent Macroeconomic Policy Effects: A Varying-Coefficient VAR

A. Ochs, C. Roerig

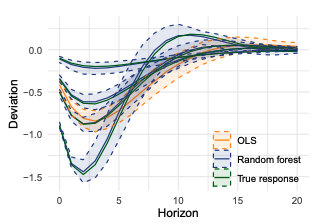

This article proposes a flexible framework to identify state-dependent effects of macroeconomic policies. In the literature, it is common to either estimate constant policy effects or introduce state-dependency in a parametric fashion. This, however, demands prior assumptions about the functional form. Our new method allows to identify state-dependent effects and possible interactions in a data-driven way. Specifically, we estimate heterogeneous policy effects using semi-parametric varying-coefficient models in an otherwise standard VAR structure. While keeping a parametric reduced form for interpretability and efficiency, we estimate the coefficients as functions of modifying macroeconomic variables, using random forests as the underlying non-parametric estimator. Simulation studies show that this method correctly identifies multiple states even for relatively small sample sizes. To further validate our method, we apply the semi-parametric framework to the historical data set by Ramey & Zubairy (2018) and offer a more granular perspective on the dependence of the fiscal policy efficacy on unemployment and interest rates.